Page 119 - CCB_Full-Annual-Report-2021

P. 119

118 Notes to the Financial Statements 119

£’000 2021 Credit rating 2020 Credit rating The Bank continues to pre-position eligible loan collateral with the Bank of England to enable it to access,

if required, the Bank of England’s Sterling Monetary Framework facilities, including the Discount Window

Cash and balances at central banks 240,158 P1/Aa3 190,962 P1/Aa3

Facility (DWF). Contents

Deposits at other banks 12,293 P1/A1 9,687 P1/A1

The Bank monitors its liquidity risk using several metrics including the liquidity coverage ratio (LCR), its loan to

Contents

European Investment Bank Bond 17,184 P1/Aaa 17,770 P1/Aaa deposits ratio (LDR) and an internal survival days metric. The Bank’s LCR at 31 December 2021 was 287% (2020:

419%) and the LDR was 95% (2020: 90%).

International Bank Reconstruction and 19,953 P1/Aaa 20,274 P1/Aaa

Development Bonds

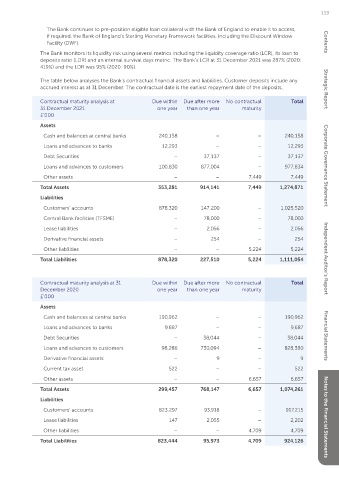

The table below analyses the Bank’s contractual financial assets and liabilities. Customer deposits include any

Derivatives held for risk management purposes (253) P1/A2 9 P2/A3 accrued interest as at 31 December. The contractual date is the earliest repayment date of the deposits. Strategic Report

Contractual maturity analysis at Due within Due after more No contractual Total

The Bank’s loans and advances to banks and debt Regular liquidity stress testing is conducted across a 31 December 2021 one year than one year maturity

securities credit risk is managed through a series of variety of scenarios covering both normal and more £’000

policies and procedures including: severe market conditions. The scenarios are developed

taking into account both Bank-specific events (e.g. a Assets

– Cash placements – Credit risk of counterparties is negative media comment) and market-related events Cash and balances at central banks 240,158 – – 240,158

controlled through the counterparty placements (e.g. prolonged market illiquidity, reduced fundability of Loans and advances to banks 12,293 – – 12,293

policy, which limits the maximum exposure by currencies, natural disasters or other catastrophes).

entity where the Bank can place cash deposits. Debt Securities – 37,137 – 37,137

The Bank’s key liquidity risk management drivers include

– Debt securities – As part of the Bank’s liquidity the following items: Loans and advances to customers 100,830 877,004 – 977,834 Corporate Governance Statement

buffer, it holds a portfolio of debt securities. The

Bank’s internal Asset and Liability Management – Deposit funding risk Other assets – – 7,449 7,449

Policy sets limits on the value and type of Total Assets 353,281 914,141 7,449 1,274,871

exposures within which the Bank’s Treasury The deposit funding risk is the primary liquidity risk

function operate. driver for the Bank. This could occur if there was Liabilities

a concern by depositors over the current or future Customers’ accounts 878,320 147,200 – 1,025,520

– Derivatives – Credit risk on derivatives is credit worthiness of the Bank. The Bank mitigates

controlled through a policy of only entering into this risk with a high proportion of its deposits being Central Bank facilities (TFSME) – 78,000 – 78,000

contracts with a limited number of UK credit protected by the UK Government’s Financial Services

institutions, with a credit rating of at least BAA Compensation Scheme (FSCS) and by having a Lease liabilities – 2,056 – 2,056

(using Moody’s long-term rating) at inception. Derivative financial assets – 254 – 254

diversified mix of deposit accounts with varying

maturity profiles. Other liabilities – – 5,224 5,224

– Pipeline loan commitments Total Liabilities 878,320 227,510 5,224 1,111,054 Independent Auditor’s Report

• Liquidity risk

The Bank needs to maintain liquidity to cover the

Liquidity risk is the risk of being unable to fund outstanding pipeline of loan offers. Although certain

assets and meet obligations as they fall due without pipeline offers may not be legally binding, the failure Contractual maturity analysis at 31 Due within Due after more No contractual Total

incurring unacceptable losses. to adhere to an expression of intent to finance a loan December 2020 one year than one year maturity

brings reputation risk, therefore liquidity is held for £’000

The Bank’s Board of Directors sets the Bank’s such pipeline offers. Assets

strategy for managing liquidity risk and delegates – Contingency funding plan

responsibility for oversight of the implementation Cash and balances at central banks 190,962 – – 190,962

of this policy to the Assets & Liabilities Committee The Bank is required to maintain a Resolution, Loans and advances to banks 9,687 – – 9,687

(ALCO). ALCO manages the Bank’s liquidity policies Recovery and Liquidity Funding Contingency Plan

and procedures mandated by the Board’s Risk & documents by its Regulator, the PRA. The plans Debt Securities – 38,044 – 38,044 Financial Statements

Compliance Committee. The Bank’s liquidity position involve a two-stage process, covering preventive Loans and advances to customers 98,286 730,094 – 828,380

is monitored on a day-to-day basis and a summary measures and corrective measures to be invoked

report, including any exceptions and remedial action when a potential or actual risk to the Bank’s liquidity Derivative financial assets – 9 – 9

taken, is provided to management daily. or capital position arises from either an internal

or external event. The plans set out what actions Current tax asset 522 – – 522

The Bank’s approach to managing liquidity is to the Bank would take to ensure it complies with the Other assets – – 6,657 6,657

ensure, as far as possible, that it will always have liquidity adequacy rules and operate within its risk

Sufficient liquidity to meet its liabilities when they appetite and limits set by the Board. Total Assets 299,457 768,147 6,657 1,074,261

fall due, under both normal and stressed conditions, – Sterling Monetary Framework facilities Liabilities

without incurring unacceptable losses, or risking

damage to the Bank’s reputation. The Bank is a participant in the Bank of England’s Customers’ accounts 823,297 93,918 – 917,215

Sterling Monetary Framework facilities. In 2021 the Lease liabilities 147 2,055 – 2,202 Notes to the Financial Statements

The Bank maintains a portfolio of short-term Bank repaid the £57m of Treasury bills drawn under

liquid assets, largely made up of short-term liquid the Funding for Lending Scheme (FLS). The Bank has Other liabilities – – 4,709 4,709

investment securities, loans and advances to also drawn £78m of funding in the form of cash under Total Liabilities 823,444 95,973 4,709 924,126

banks and other inter-bank facilities, to ensure that the Bank of England’s TFSME scheme (Term Funding

sufficient liquidity is maintained. Scheme with additional incentives for SME) in 2021.