Page 97 - CCB_Full-Annual-Report-2021

P. 97

96 Notes to the Financial Statements 97

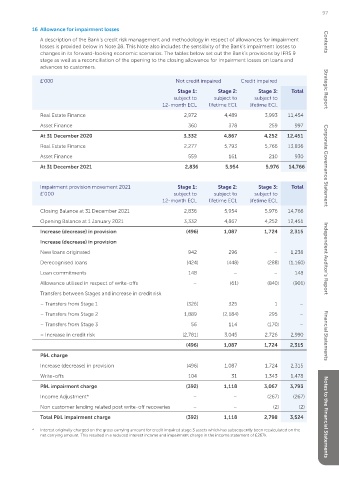

The Bank has measured its loans and advances to Gross loans and advances to customers includes Hire 16 Allowance for impairment losses

customers at amortised cost on the basis that the Purchase and Finance Lease agreements. The table A description of the Bank’s credit risk management and methodology in respect of allowances for impairment

Bank holds these assets for the objective of collecting below shows the timing of the expected cashflows losses is provided below in Note 28. This Note also includes the sensitivity of the Bank’s impairment losses to Contents

contractual cash flows, and the cash flows associated on these agreements. changes in its forward-looking economic scenarios. The tables below set out the Bank’s provisions by IFRS 9

Contents

with the assets include only payments of principal stage as well as a reconciliation of the opening to the closing allowance for impairment losses on loans and

and interest (SPPI). £’000 2021 2020

advances to customers.

Gross investment in finance

For the purposes of this assessment, ‘principal’ is lease receivables*: £’000 Not credit impaired Credit impaired

defined as the fair value of the financial asset on initial

recognition. ‘Interest’ is defined as consideration for Less than one year 29,317 21,686 Stage 1: Stage 2: Stage 3: Total Strategic Report

the time value of money for the credit risk associated 1 – 2 Years 23,903 17,260 subject to subject to subject to

with the principal amount outstanding during a 12-month ECL lifetime ECL lifetime ECL

particular period and for other basic lending risks and 2 – 3 Years 17,906 15,081 Real Estate Finance 2,972 4,489 3,993 11,454

costs, as well as a profit margin.

3 – 4 Years 13,123 9,941

Asset Finance 360 378 259 997

In making this assessment the Bank has considered 4 – 5 Years 9,739 7,069 At 31 December 2020 3,332 4,867 4,252 12,451

whether the financial asset contains a contractual

term that could change the timing or amount More than five years 10,756 8,935 Real Estate Finance 2,277 5,793 5,766 13,836

of contractual cashflows such that it would not Total 104,744 79,972

meet this condition. All the Bank’s loans contain Asset Finance 559 161 210 930

prepayment features. A prepayment feature is Unearned future finance (13,900) (11,440) At 31 December 2021 2,836 5,954 5,976 14,766 Corporate Governance Statement

consistent with the SPPI criteria if the prepayment income on finance charges

amount substantially represents unpaid amounts Net investment in 90,844 68,532

of principal and interest on the principal amount finance leases Impairment provision movement 2021 Stage 1: Stage 2: Stage 3: Total

outstanding, which may include reasonable £’000 subject to subject to subject to

compensation for early termination of the contract. The net investment in 12-month ECL lifetime ECL lifetime ECL

finance leases may be

analysed as follows: Closing Balance at 31 December 2021 2,836 5,954 5,976 14,766

Gross loans and advances is net of an EIR liability of

£4.1m (2020: £3.1m). Less than one year 24,500 17,731 Opening Balance at 1 January 2021 3,332 4,867 4,252 12,451

Between one and five years 56,635 42,685 Increase (decrease) in provision (496) 1,087 1,724 2,315

£’000 2021 2020

More than five years 9,709 8,116 Increase (decrease) in provision

Gross loans and advances 992,600 840,831

90,844 68,532 New loans originated 942 296 – 1,238

Less: allowance for (14,766) (12,451) Independent Auditor’s Report

impairment losses Derecognised loans (424) (448) (288) (1,160)

(see Note 16) *Excludes effective interest rate

Loan commitments 148 – – 148

Net loan receivables 977,834 828,380

Allowance utilised in respect of write-offs – (61) (840) (901)

Transfers between Stages and increase in credit risk

– Transfers from Stage 1 (326) 325 1 –

– Transfers from Stage 2 1,889 (2,184) 295 –

– Transfers from Stage 3 56 114 (170) –

– Increase in credit risk (2,781) 3,045 2,726 2,990 Financial Statements

(496) 1,087 1,724 2,315

P&L charge

Increase (decrease) in provision (496) 1,087 1,724 2,315

Write-offs 104 31 1,343 1,478

P&L impairment charge (392) 1,118 3,067 3,793

Income Adjustment* – – (267) (267)

Non customer lending related post write-off recoveries – – (2) (2)

Total P&L impairment charge (392) 1,118 2,798 3,524 Notes to the Financial Statements

* Interest originally charged on the gross carrying amount for credit impaired stage 3 assets which has subsequently been recalculated on the

net carrying amount. This resulted in a reduced interest income and impairment charge in the income statement of £267k.