Page 94 - CCB_Annual Report_2022

P. 94

94 Notes to the Financial Statements 95

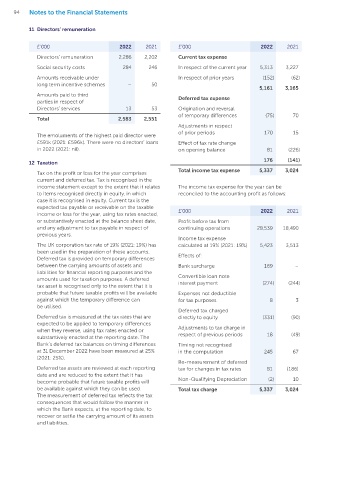

11 Directors’ remuneration • Deferred tax

Deferred tax assets are attributable as follows:

£’000 2022 2021 £’000 2022 2021

The Bank had a deferred tax asset of £1,099k at 31 December 2022 (2021: £775k) resulting primarily from the

Directors’ remuneration 2,286 2,202 Current tax expense original adoption of IFRS accounting standards in 2015, and more recently IFRS 9. The business plan projects

profits in future years sufficient to recognise this asset.

Social security costs 284 246 In respect of the current year 5,313 3,227

Amounts receivable under In respect of prior years (152) (62) Balance Sheet Movement in period

long term incentive schemes – 50

5,161 3,165

Amounts paid to third Deferred tax expense £’000 2022 2021 Income Equity

parties in respect of Deferred tax liability

Directors’ services 13 53 Origination and reversal Plant, Property & Equipment (PPE) and intangible assets – (18) 18 –

of temporary differences (75) 70

Total 2,583 2,551 Total Liabilities – (18) 18 –

Adjustments in respect

of prior periods 170 15 Deferred tax asset

The emoluments of the highest paid director were

£591k (2021: £596k). There were no directors’ loans Effect of tax rate change Deductible temporary differences

in 2022 (2021: nil). on opening balance 81 (226)

Pension and other remuneration benefits 163 (163) –

12 Taxation 176 (141) IFRS 9 transitional relief 454 545 (91) –

Total income tax expense 5,337 3,024

Tax on the profit or loss for the year comprises Plant, Property & Equipment (PPE) and intangible assets 121 – 121 –

current and deferred tax. Tax is recognised in the

income statement except to the extent that it relates The income tax expense for the year can be Other 120 180 (60) –

to items recognised directly in equity, in which reconciled to the accounting profit as follows: Total Assets 695 888 (193) –

case it is recognised in equity. Current tax is the

expected tax payable or receivable on the taxable £’000 2022 2021 Deferred tax on fair value through other

income or loss for the year, using tax rates enacted, comprehensive income

or substantively enacted at the balance sheet date, Profit before tax from FVOCI instruments 404 (95) – (499)

and any adjustment to tax payable in respect of continuing operations 28,539 18,490

previous years. Net deferred tax asset 1,099 775 (175) (499)

Income tax expense

The UK corporation tax rate of 19% (2021: 19%) has calculated at 19% (2021: 19%) 5,423 3,513

been used in the preparation of these accounts. Effects of:

Deferred tax is provided on temporary differences

between the carrying amounts of assets and Bank surcharge 169 – 13 Cash and cash equivalents 14 Loans and advances to banks

liabilities for financial reporting purposes and the Convertible loan note Cash and cash equivalents include notes and coins Loans and advances to banks are measured at

amounts used for taxation purposes. A deferred interest payment (274) (244) in hand, unrestricted balances held with central amortised cost as the Bank holds these assets for

tax asset is recognised only to the extent that it is banks, and highly liquid financial assets with original the objective of collecting contractual cash flows,

probable that future taxable profits will be available Expenses not deductible maturities of three months or less from the date of and the cash flows associated with the assets

against which the temporary difference can for tax purposes 8 3 acquisition, that are subject to an insignificant risk of include only payments of principal and interest

be utilised.

Deferred tax charged change in their fair value and are used by the Bank (SPPI). As with loans and advances to customers

Deferred tax is measured at the tax rates that are directly to equity (331) (90) in the management of its short-term commitments. (Note 15), the Bank has assessed whether there

expected to be applied to temporary differences Cash and cash equivalents are carried at amortised are any contractual terms which may cause the

when they reverse, using tax rates enacted or Adjustments to tax charge in cost in the statement of financial position. financial assets to fail the SPPI test. The Bank has

substantively enacted at the reporting date. The respect of previous periods 18 (49) noted no such terms. The Bank does not incur any

Bank’s deferred tax balances on timing differences Timing not recognised £’000 2022 2021 transactional or other such integral fees which

at 31 December 2022 have been measured at 25% in the computation 245 67 require an effective interest rate to be specifically

(2021: 25%). Unrestricted balances calculated for these assets. Income is recognised at

Re-measurement of deferred with central banks* 286,680 240,158 the contractual interest rate on an accruals basis

Deferred tax assets are reviewed at each reporting tax for changes in tax rates 81 (186)

date and are reduced to the extent that it has Cash and balances

become probable that future taxable profits will Non-Qualifying Depreciation (2) 10 with other banks 13,931 12,293 £’000 2022 2021

be available against which they can be used. Total tax charge 5,337 3,024

The measurement of deferred tax reflects the tax Total 300,611 252,451 Gross loans and

consequences that would follow the manner in * Included within the unrestricted balances with central banks is advances to banks 13,931 12,293

which the Bank expects, at the reporting date, to £447k of accrued interest for 2022 (2021: £24k) Net loans and

recover or settle the carrying amount of its assets advances to banks 13,931 12,293

and liabilities.