Page 121 - CCB_Annual Report_2022

P. 121

120 Notes to the Financial Statements 121

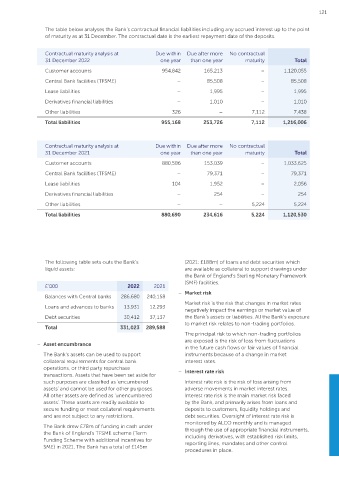

The Bank continues to pre-position eligible loan collateral with the Bank of England to enable it to access, The table below analyses the Bank’s contractual financial liabilities including any accrued interest up to the point

if required, the Bank of England’s Sterling Monetary Framework facilities, including the Discount Window of maturity as at 31 December. The contractual date is the earliest repayment date of the deposits.

Facility (DWF).

The Bank monitors its liquidity risk using several metrics including the liquidity coverage ratio (LCR), its loan Contractual maturity analysis at Due within Due after more No contractual

to deposits ratio (LDR) and an internal survival days metric. The Bank’s LCR at 31 December 2022 was 361% 31 December 2022 one year than one year maturity Total

(2021: 287%) and the LDR was 94% (2021: 95%).

Customer accounts 954,842 165,213 – 1,120,055

The table below analyses the Bank’s contractual financial assets and liabilities. Customer deposits include any Central Bank facilities (TFSME) – 85,508 – 85,508

accrued interest as at 31 December. The contractual date is the earliest repayment date of the deposits.

Lease liabilities – 1,995 – 1,995

Contractual maturity analysis at Derivatives financial liabilities – 1,010 – 1,010

31 December 2022 Due within Due after more No contractual Other liabilities 326 – 7,112 7,438

£’000 one year than one year maturity Total

Total liabilities 955,168 253,726 7,112 1,216,006

Assets

Cash and balances at central banks 286,680 – – 286,680

Loans and advances to banks 13,931 – – 13,931 Contractual maturity analysis at Due within Due after more No contractual

31 December 2021 one year than one year maturity Total

Debt Securities 19,699 10,713 – 30,412

Customer accounts 880,586 153,039 – 1,033,625

Loans and advances to customers 92,512 945,198 – 1,037,710

Central Bank facilities (TFSME) – 79,371 – 79,371

Other assets – – 7,812 7,812

Lease liabilities 104 1,952 – 2,056

Total Assets 412,822 955,911 7,812 1,376,545

Derivatives financial liabilities – 254 – 254

Liabilities

Other liabilities – – 5,224 5,224

Customers’ accounts 948,438 154,818 – 1,103,256

Total liabilities 880,690 234,616 5,224 1,120,530

Central Bank facilities (TFSME) – 78,000 – 78,000

Lease liabilities – 1,995 – 1,995

Derivative financial liabilities – 1,010 – 1,010

Other Liabilities 326 – 7,112 7,438

Total liabilities 948,764 235,823 7,112 1,191,699

The following table sets outs the Bank’s (2021: £188m) of loans and debt securities which

liquid assets: are available as collateral to support drawings under

the Bank of England’s Sterling Monetary Framework

Contractual maturity analysis at £’000 2022 2021 (SMF) facilities.

31 December 2021 Due within Due after more No contractual – Market risk

£’000 one year than one year maturity Total Balances with Central banks 286,680 240,158

Market risk is the risk that changes in market rates

Assets Loans and advances to banks 13,931 12,293

negatively impact the earnings or market value of

Cash and balances at central banks 240,158 – – 240,158 Debt securities 30,412 37,137 the Bank’s assets or liabilities. All the Bank’s exposure

to market risk relates to non-trading portfolios.

Loans and advances to banks 12,293 – – 12,293 Total 331,023 289,588

The principal risk to which non-trading portfolios

Debt Securities – 37,137 – 37,137

– Asset encumbrance are exposed is the risk of loss from fluctuations

Loans and advances to customers 100,830 877,004 – 977,834 in the future cash flows or fair values of financial

The Bank’s assets can be used to support instruments because of a change in market

Other assets – – 7,449 7,449

collateral requirements for central bank interest rates.

Total Assets 353,281 914,141 7,449 1,274,871 operations, or third party repurchase – Interest rate risk

transactions. Assets that have been set aside for

Liabilities

such purposes are classified as ‘encumbered Interest rate risk is the risk of loss arising from

Customers’ accounts 878,320 147,200 – 1,025,520 assets’ and cannot be used for other purposes. adverse movements in market interest rates.

All other assets are defined as ‘unencumbered Interest rate risk is the main market risk faced

Central Bank facilities (TFSME) – 78,000 – 78,000

assets’. These assets are readily available to by the Bank, and primarily arises from loans and

Lease liabilities – 2,056 – 2,056 secure funding or meet collateral requirements deposits to customers, liquidity holdings and

and are not subject to any restrictions. debt securities. Oversight of interest rate risk is

Derivative financial liabilities – 254 – 254 monitored by ALCO monthly and is managed

The Bank drew £78m of funding in cash under

Other Liabilities – – 5,224 5,224 through the use of appropriate financial instruments,

the Bank of England’s TFSME scheme (Term

including derivatives, with established risk limits,

Total liabilities 878,320 227,510 5,224 1,111,054 Funding Scheme with additional incentives for reporting lines, mandates and other control

SME) in 2021. The Bank has a total of £145m

procedures in place.