Page 115 - CCB_Annual Report_2022

P. 115

114 Notes to the Financial Statements 115

Under IFRS 9 customers may move from a stage 1 – the remaining lifetime PD at the reporting date Forbearance analysis

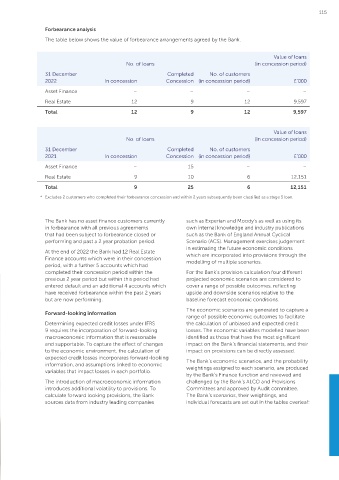

provision exposure to a stage 2 exposure as a result based on the modified terms; with The table below shows the value of forbearance arrangements agreed by the Bank.

of a significant increase in credit risk. To determine – the remaining lifetime PD estimated based

whether the credit risk on a particular financial on data on initial recognition and the original

instrument has increased significantly since initial contractual terms. Value of loans

recognition the Bank reviews each account annually, No. of loans (in concession period)

or more regularly, should the customer’s payment Should modification result in a derecognition 31 December Completed No. of customers

record show any deterioration. event, the Bank would make an assessment as to

whether the new financial asset is credit impaired at 2022 In concession Concession (in concession period) £’000

As a backstop, and as required by IFRS 9, the Bank initial recognition. Asset Finance – – – –

will presumptively consider that a significant increase

in credit risk occurs no later than when an asset is Forbearance can be temporary or permanent Real Estate 12 9 12 9,597

more than 30 days past due. depending on the circumstances, progress

on rehabilitation, and the detail of the Total 12 9 12 9,597

For an account to be ‘cured’ i.e. evidence a concession agreed.

significant reduction in credit risk, and return from

stage 2 to stage 1, the customer would need to Forbearance – curing Value of loans

demonstrate a good track record of payments. No. of loans (in concession period)

Loans are classified as forborne at the time

Movement from stage 3 to stage 2 will only occur a customer in financial difficulty is granted 31 December Completed No. of customers

when the borrower satisfies all the criteria in the a concession. 2021 In concession Concession (in concession period) £’000

table above.

The customer will remain treated and recorded as Asset Finance – 15 – –

All staging classifications are subject to management forborne until the following exit conditions are met: Real Estate 9 10 6 12,151

review and can be overridden subject to

appropriate approval at the Bank’s Provision or – When all due payments, as per the amended Total 9 25 6 12,151

Credit Committees. contractual terms, have been made in a timely

manner over a continuous repayment period * Excludes 2 customers who completed their forbearance concession and within 2 years subsequently been classified as a stage 3 loan.

Forbearance (loan is considered as performing);

The Bank can implement forbearance agreements – A minimum two-year probation period has The Bank has no asset finance customers currently such as Experian and Moody’s as well as using its

for the servicing and management of customers passed from the date the forborne exposure was in forbearance with all previous agreements own internal knowledge and industry publications

who are in financial difficulty and require some form considered as performing; that had been subject to forbearance closed or such as the Bank of England Annual Cyclical

of concession to be granted, even if this concession – None of the customer’s exposures are more performing and past a 2 year probation period. Scenario (ACS). Management exercises judgement

entails a loss for the Bank. A concession may be than 30 days past due at the end of the in estimating the future economic conditions

either a modification of the previous terms and probation period. At the end of 2022 the Bank had 12 Real Estate which are incorporated into provisions through the

conditions of an agreement, which the borrower is Finance accounts which were in their concession modelling of multiple scenarios.

considered unable to comply with due to financial period, with a further 5 accounts which had

difficulties, or a total or partial refinancing of an completed their concession period within the For the Bank’s provision calculation four different

agreement that would not have been granted had previous 2 year period but within this period had projected economic scenarios are considered to

the borrower not been in financial difficulties. entered default and an additional 4 accounts which cover a range of possible outcomes, reflecting

have received forbearance within the past 2 years upside and downside scenarios relative to the

The Bank may modify the contractual terms of but are now performing. baseline forecast economic conditions.

a loan for several reasons, including to reflect

changing market conditions, or where forbearance Forward‑looking information The economic scenarios are generated to capture a

(i.e. a renegotiation of the terms of a loan) is granted range of possible economic outcomes to facilitate

at the request of a borrower. This modification may Determining expected credit losses under IFRS the calculation of unbiased and expected credit

have an impact on the IFRS 9 impairment provision 9 requires the incorporation of forward-looking losses. The economic variables modelled have been

stage to which the asset is allocated. macroeconomic information that is reasonable identified as those that have the most significant

and supportable. To capture the effect of changes impact on the Bank’s financial statements, and their

An existing loan whose terms have been modified to the economic environment, the calculation of impact on provisions can be directly assessed.

may require derecognition, and the renegotiated expected credit losses incorporates forward-looking

loan recognised as a new loan at fair value, with any information, and assumptions linked to economic The Bank’s economic scenarios, and the probability

adjustments taken through the income statement. variables that impact losses in each portfolio. weightings assigned to each scenario, are produced

Derecognition is assessed using the same ’10 by the Bank’s Finance function and reviewed and

percent’ test applied to financial liabilities. Where a The introduction of macroeconomic information challenged by the Bank’s ALCO and Provisions

modification does not result in derecognition, the introduces additional volatility to provisions. To Committees and approved by Audit committee.

gross carrying amount of the asset is recalculated calculate forward looking provisions, the Bank The Bank’s scenarios, their weightings, and

as the present value of the modified cash flows, sources data from industry leading companies individual forecasts are set out in the tables overleaf:

discounted at the financial assets original effective

interest rate. Any subsequent modification gain or

loss is then recognised in the profit or loss amount.

When the terms of a financial asset are modified, and

the modification does not result in derecognition,

the determination of whether the asset’s credit risk

has increased significantly reflects comparisons of: