Page 34 - CCB_Annual Report_2022

P. 34

34 Strategic Report 35

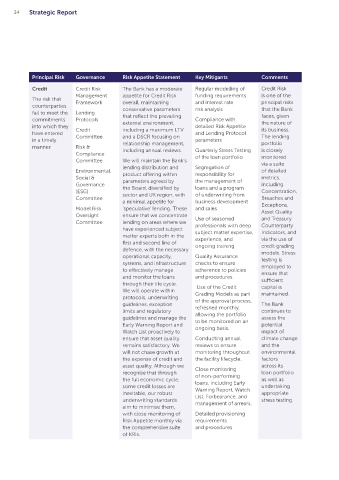

Principal Risk Governance Risk Appetite Statement Key Mitigants Comments Principal Risk Governance Risk Appetite Statement Key Mitigants Comments

Credit Credit Risk The Bank has a moderate Regular modelling of Credit Risk Legal, Compliance The Bank maintains a Compliance monitoring Ensuring

Management appetite for Credit Risk funding requirements is one of the Compliance Framework low appetite for Legal, of the Bank’s activities compliance

The risk that Framework overall, maintaining and interest rate principal risks & Regulatory Compliance and Regulatory through an approved with all

counterparties conservative parameters risk analysis that the Bank Data Protection Risk. Whilst we recognise annual plan applicable

fail to meet the Lending that reflect the prevailing faces, given The risk Framework that operational errors can regulatory

commitments Protocols external environment, Compliance with the nature of that non- Compliance occur, we maintain zero Undertaking detailed and requirements in

into which they Credit including a maximum LTV detailed Risk Appetite its business. compliance Monitoring tolerance for reportable regular reviews of key a fast-changing

have entered Committee and a DSCR focusing on and Lending Protocol The lending with laws or Framework breaches of regulations, activities and processes landscape is

in a timely relationship management, parameters portfolio regulations regulatory policy breaches, via the second line a challenge

manner. Risk & including annual reviews. Quarterly Stress Testing is closely could give Risk breaches of applicable laws, oversight programme to which the

Compliance of the loan portfolio monitored rise to fines, Management late responses to regulatory Provision of guidance Bank devotes

Committee We will maintain the Bank’s via a suite litigation, Committee requests. We strive to in relation to business, considerable

lending distribution and Segregation of sanctions,

Environmental, product offering within responsibility for of detailed reputational Risk & ensure that we always product, and change resources, and

Social & parameters agreed by the management of metrics, damage or Compliance remain within the law and management requests. the Compliance

Governance the Board, diversified by loans and a program including financial loss. Committee regulation. Regulatory Ensuring appropriate and Data

(ESG) sector and UK region, with of underwriting from Concentration, Changes (Horizon registrations under the Protection

Committee Breaches and Scanning) are logged, Frameworks

a minimal appetite for business development Exceptions, Senior Management

Model Risk ‘speculative’ lending. These and sales Asset Quality allocated, monitored, and and Certification are continually

under review

tracked ensuring additions

Oversight ensure that we concentrate Use of seasoned and Treasury to or changes within Regime through second to ensure that

Committee lending on areas where we professionals with deep Counterparty regulatory requirements line oversight they meet all

have experienced subject subject matter expertise, Indicators, and are proportionately applied. Maintaining logs of requirements

matter experts both in the experience, and via the use of All material breaches internal compliance and is in line

first and second line of ongoing training credit grading are investigated and breaches, regulatory with leading

defence, with the necessary models. Stress reported to the Risk & breaches and conflicts industry

operational capacity, Quality Assurance testing is Compliance Committee of interest practices.

systems, and infrastructure checks to ensure employed to in a timely manner, and

to effectively manage adherence to policies ensure that staff operate within the Horizon scanning Annual

and monitor the loans and procedures. sufficient Bank’s documented to ensure continued submission

through their life cycle. Use of the Credit capital is policies and controls adherence to regulatory of the Data

We will operate within Grading Models as part maintained. and, where applicable, requirements Protection

protocols, underwriting of the approval process, industry guidelines. and developments. Officers’ Report.

guidelines, exception refreshed monthly, The Bank Regular reviews of Approval of

limits and regulatory allowing the portfolio continues to training content and the Annual

guidelines and manage the to be monitored on an assess the oversight of the training Compliance

Early Warning Report and ongoing basis. potential and development of Monitoring Plan.

Watch List proactively to impact of staff to ensure up to date

ensure that asset quality Conducting annual climate change knowledge base.

remains satisfactory. We reviews to ensure and the

will not chase growth at monitoring throughout environmental Executive owned KRIs.

the expense of credit and the facility lifecycle. factors

asset quality. Although we Close monitoring across its

recognise that through of non-performing loan portfolio

the full economic cycle, loans, including Early as well as

some credit losses are Warning Report, Watch undertaking

inevitable, our robust List, Forbearance, and appropriate

underwriting standards management of arrears. stress testing.

aim to minimise them,

with close monitoring of Detailed provisioning

Risk Appetite monthly via requirements

the comprehensive suite and procedures

of KRIs.