Page 101 - CCB_Annual Report_2022

P. 101

100 Notes to the Financial Statements 101

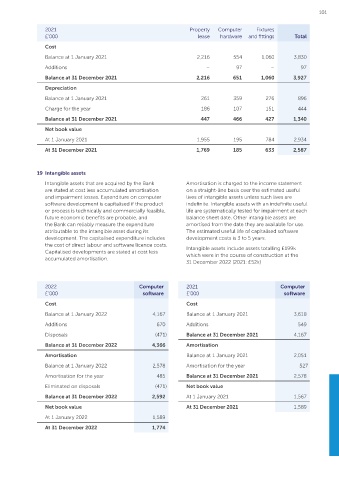

17 Debt securities 2021 Property Computer Fixtures

£’000 lease hardware and fittings Total

Under IFRS 9 the Bank’s debt securities are measured accumulated in equity, together with the tax

at fair value through other comprehensive income. thereon, is reclassified to the income statement. Cost

The Bank’s debt securities are initially recognised During 2022 an EIB bond with a nominal value of Balance at 1 January 2021 2,216 554 1,060 3,830

at fair value and subsequently measured at fair £10m matured and has not been replaced. Additions – 97 – 97

value through other comprehensive income. The

instruments meet the SPPI criteria but as the assets £’000 2022 2021 Balance at 31 December 2021 2,216 651 1,060 3,927

are in a Held To Collect and Sell Business Model they Depreciation

are recorded at Fair Value with changes recorded European Investment

through Other Comprehensive Income (OCI). Bank bond (EIB) 10,713 17,184 Balance at 1 January 2021 261 359 276 896

Changes in the fair value of debt securities are International Bank Charge for the year 186 107 151 444

recognised in other comprehensive income Reconstruction &

and presented in the fair value through other Development bond (IBRD) 19,699 19,953 Balance at 31 December 2021 447 466 427 1,340

comprehensive income reserve. When the debt Total 30,412 37,137 Net book value

security is sold or matures, the gain or loss

At 1 January 2021 1,955 195 784 2,934

At 31 December 2021 1,769 185 633 2,587

18 Property, plant and equipment 19 Intangible assets

Property, plant and equipment are stated at cost Depreciation is charged to the income Intangible assets that are acquired by the Bank Amortisation is charged to the income statement

less accumulated depreciation and accumulated statement on a straight-line basis over the are stated at cost less accumulated amortisation on a straight-line basis over the estimated useful

impairment losses. Where parts of an item of estimated useful lives of each part of an item. and impairment losses. Expenditure on computer lives of intangible assets unless such lives are

property, plant and equipment have different useful The estimated useful lives are as follows: software development is capitalised if the product indefinite. Intangible assets with an indefinite useful

lives, they are accounted for as separate items of – Leasehold properties 2 – 15 years or process is technically and commercially feasible, life are systematically tested for impairment at each

property, plant, and equipment. future economic benefits are probable, and balance sheet date. Other intangible assets are

– Computer hardware 1 – 5 years the Bank can reliably measure the expenditure amortised from the date they are available for use.

Leases in which the Bank assumes substantially all attributable to the intangible asset during its The estimated useful life of capitalised software

the risks and rewards of ownership of the leased – Fixtures and fittings 3 – 10 years development. The capitalised expenditure includes development costs is 3 to 5 years.

asset are classified as finance leases and are stated at The Bank’s depreciation methods, useful the cost of direct labour and software licence costs.

the amount equal to the lower of their fair value and lives, and residual values are reviewed at each Capitalised developments are stated at cost less Intangible assets include assets totalling £199k

the present value of the minimum lease payments at balance sheet date. accumulated amortisation. which were in the course of construction at the

inception of the lease, less accumulated depreciation. 31 December 2022 (2021: £52k)

2022 Property Computer Fixtures 2022 Computer 2021 Computer

£’000 lease hardware and fittings Total £’000 software £’000 software

Cost Cost Cost

Balance at 1 January 2022 2,216 651 1,060 3,927 Balance at 1 January 2022 4,167 Balance at 1 January 2021 3,618

Additions 52 148 – 200 Additions 670 Additions 549

Disposals (116) – – (116) Disposals (471) Balance at 31 December 2021 4,167

Balance at 31 December 2022 2,152 799 1,060 4,011 Balance at 31 December 2022 4,366 Amortisation

Depreciation Amortisation Balance at 1 January 2021 2,051

Balance at 1 January 2022 447 466 427 1,340 Balance at 1 January 2022 2,578 Amortisation for the year 527

Charge for the year 151 119 151 421 Amortisation for the year 485 Balance at 31 December 2021 2,578

Eliminated on disposals (116) – – (116) Eliminated on disposals (471) Net book value

Balance at 31 December 2022 482 585 578 1,645 Balance at 31 December 2022 2,592 At 1 January 2021 1,567

Net book value Net book value At 31 December 2021 1,589

At 1 January 2022 1,769 185 633 2,587 At 1 January 2022 1,589

At 31 December 2022 1,670 214 482 2,366 At 31 December 2022 1,774